If you’ve been dreaming of building a barndominium, you’ve probably already done the fun part — browsing floor plans, pricing out steel kits, and picturing that open-concept living room with 18-foot ceilings. Then comes the less glamorous question that stops a lot of would-be barndo owners in their tracks: how do I actually pay for this thing?

Barndominium financing is genuinely different from financing a traditional stick-built home, and not every lender knows how to handle it. The good news is that in 2026, your options are broader than ever. Government-backed loans, Farm Credit lenders, construction-to-permanent loans, and conventional mortgages can all potentially be used — depending on your location, credit score, down payment, and how the property is structured.

This guide walks you through every major barndominium financing option available to US buyers right now, explains what lenders actually look for, tells you which loan fits which situation, and points you to tools that make the math easy before you ever walk into a bank.

Quick Start: Already know your build cost? Use our free barndominium financing calculator to estimate your monthly payments, construction-phase interest, and total project cost by state — in under two minutes.

What Makes Barndominium Financing Different?

Before diving into loan types, it helps to understand why barndominiums create friction with traditional lenders.

The core issue is appraisal. When a conventional lender approves a mortgage, they need a comparable-sales appraisal — meaning they look at similar homes that sold nearby to confirm your property is worth what you’re paying. In most rural areas, there simply aren’t enough sold barndominiums to produce reliable comps. That makes some lenders nervous.

The second issue is non-standard construction. A steel post-frame building doesn’t look like a standard residential property to an underwriter who has never seen one. Some lenders incorrectly classify barndominiums as agricultural or commercial structures, which triggers different — and often much stricter — lending rules.

The third issue is draw schedules. Unlike a traditional home purchase where you get one loan for one finished property, building a barndominium usually involves a construction-to-permanent loan — a two-phase product where funds are released in draws as the build progresses. Not every lender offers these, and the ones that do have different requirements.

None of these issues are dealbreakers. They just mean you need to find the right lender and come prepared with the right documentation.

The 5 Main Barndominium Financing Options

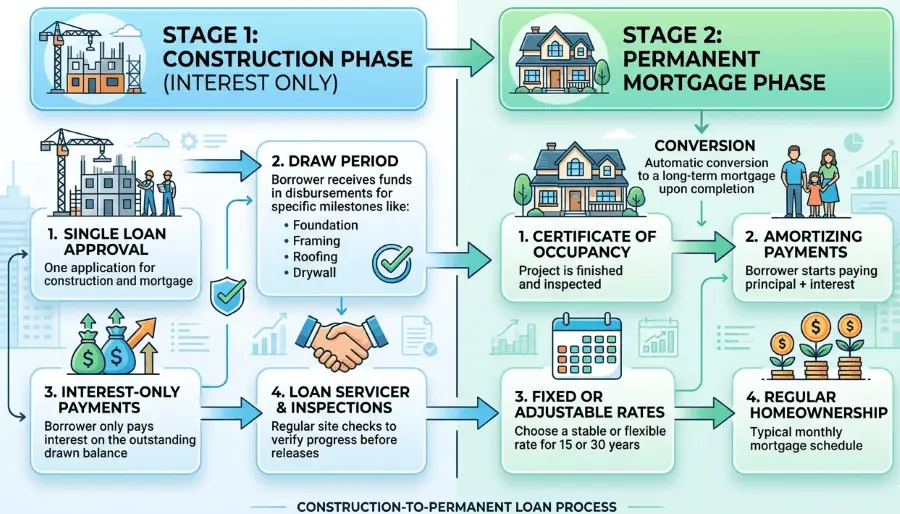

1. Construction-to-Permanent Loan (Most Common)

This is the workhorse of barndominium financing and the option most builders will point you toward.

A construction-to-permanent (C2P) loan works in two stages:

- Stage 1 — Construction phase: The lender releases funds in draws as your builder completes milestones (foundation poured, framing complete, rough-in done, etc.). During this phase you typically pay interest only on the amount drawn, not the full loan balance.

- Stage 2 — Permanent mortgage: Once construction is complete and the certificate of occupancy is issued, the loan automatically converts to a standard mortgage. One closing, two stages.

The major advantage is one set of closing costs. With a construction-only loan (also called a two-close loan), you’d pay closing costs twice — once at construction start and again when you refinance into a permanent mortgage. The C2P structure eliminates the second closing entirely.

Typical requirements:

- Credit score of 680+ (some lenders go down to 640)

- 10–20% down payment

- Licensed, insured general contractor

- Detailed construction budget and timeline

- Signed construction contract

Average interest rate in 2026: Construction phase rates are typically 1–2% above the permanent rate, reflecting the lender’s added risk during the build.

Want to see exactly what your construction-phase interest and permanent payment will look like? Our barndominium financing calculator models both phases side by side, including draw schedule scenarios (even, front-loaded, or back-loaded draws).

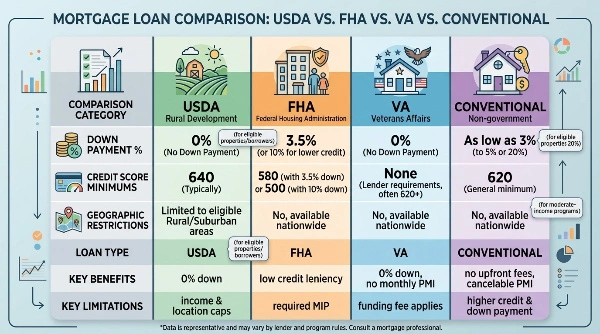

2. USDA Construction Loan (Best for Rural Buyers)

If you’re building in a rural or semi-rural area — which describes the vast majority of barndominium projects — the USDA loan program deserves your serious attention.

The United States Department of Agriculture backs home loans for eligible rural and suburban properties through its Single Family Housing programs. The headline benefit: $0 down payment. For a $350,000 barndominium, that’s a $35,000–$70,000 difference compared to a conventional loan.

USDA loans are government-backed and offer construction-to-permanent options that roll construction and long-term financing into one, making the process more straightforward than a two-close approach.

USDA barndominium requirements:

- Property must be in a USDA-eligible rural area (check the USDA property eligibility map)

- The barndominium must have a permanent, HUD-compliant foundation

- The structure must meet local building codes and be classified as a residential property

- Income limits apply (generally 115% of the area median income)

- Credit score typically 640+

One challenge with USDA barndominium financing is that not all lenders offer the construction-to-permanent option, and some lenders may not finance non-traditional home types like barndominiums at all. This is why finding a lender with specific barndominium experience is so important — and why local banks and Farm Credit lenders often outperform big national banks here.

If your land is in an eligible area and your income qualifies, USDA is often the single best barndominium financing option available. The zero-down feature alone can change the entire economics of your build.

3. FHA Construction Loan (Best for Lower Credit Scores)

The Federal Housing Administration backs loans that allow lower credit scores and smaller down payments than conventional lenders typically require.

FHA loans are available for people with less-than-perfect credit scores to purchase or build barndominiums with as little as 3.5% down with a credit score above 580, and 10% down with a credit score from 500 to 579.

For barndominium financing specifically, two FHA programs are relevant:

- FHA One-Time Close Construction Loan: Covers both the construction and permanent mortgage phases in a single closing — similar to a C2P loan. This is ideal for ground-up barndo builds.

- FHA 203(k) Rehabilitation Loan: If you’re purchasing an existing barndominium that needs significant work, this program bundles the purchase price and renovation costs into one loan.

FHA construction loans like the 203(k) and the one-time close option can fund building or renovating a barndominium, and while FHA loans may involve stricter property standards, they also offer benefits like low down payment and credit requirements.

Key FHA requirement: Construction must be carried out by a licensed contractor. You can’t use an FHA construction loan for a true owner-builder project.

Not available in rural-only areas: Unlike USDA loans, FHA loans are not geographically restricted. Whether you’re building outside of Dallas or in rural Mississippi, FHA financing can apply.

4. VA Construction Loan (Best for Veterans)

If you’re an active-duty service member, veteran, or eligible surviving spouse, the VA loan program is arguably the most powerful barndominium financing tool available.

VA loans offer $0 down payment and low-interest construction and purchase loans, with credit requirements more lenient than most conventional loan programs. VA construction loans offer up to 100% financing for qualified borrowers.

That means a veteran could potentially build a $400,000 barndominium with zero down payment, no PMI (Private Mortgage Insurance), and a competitive interest rate. The lifetime savings compared to a conventional loan can easily exceed $100,000 over a 30-year term.

VA construction loan requirements for barndominiums:

- Must be your primary residence

- The barndominium must meet VA Minimum Property Requirements (MPRs)

- Licensed builder required

- VA appraisal must confirm value

- Certificate of Eligibility required (obtain at VA.gov)

The VA appraisal can be the trickiest part for barndominium builds — appraisers may struggle with comps just as with other loan types. Working with a lender who has done VA barndominium loans before dramatically increases your chances of a smooth process.

5. Conventional Construction Loan (Most Flexible, Strictest Requirements)

Conventional loans — those not backed by a government agency — are available from banks, credit unions, and mortgage companies. They offer the most flexibility in terms of property type and loan structure, but they also have the highest credit and down payment requirements.

If a barndominium meets standard housing criteria, it may qualify for a conventional mortgage, and lenders that understand barndominium builds may treat them like stick-built homes, especially when constructed with wood framing and permanent foundations.

Conventional C2P loan typical requirements:

- Credit score 680–720+

- 10–20% down payment

- Detailed construction plans and builder credentials

- Reserves (typically 6–12 months of payments in savings)

The advantage of conventional loans is that they’re not subject to geographic restrictions (USDA) or property-type quirks (FHA inspections), and for buyers with strong credit, they often offer the lowest long-term interest rates.

Local banks and credit unions are frequently your best bet for conventional barndominium construction loans. Big national lenders often have rigid underwriting systems that auto-decline non-standard properties. A local community bank whose loan officer has seen barndominiums before can use more judgment and flexibility.

6. Farm Credit System (The Hidden Gem)

This is the option that most barndominium articles miss entirely.

The Farm Credit System is a network of lender-owned cooperatives that have been financing rural land and construction for over a century. Institutions like AgTexas Farm Credit, Farm Credit Mid-America, AgSouth Farm Credit, and others understand rural property better than almost any other lender category.

The Farm Credit System may be able to provide loans to help you purchase the land where you’d like to construct your barndominium, construct your barndominium, or both.

Because Farm Credit lenders deal with non-standard rural properties every day, they’re often much more comfortable with barndominium appraisals and construction financing than conventional lenders. They may also offer land + construction bundled financing, which can simplify the process significantly if you’re buying land and building simultaneously.

Find your regional Farm Credit lender at FarmCredit.com.

What Lenders Actually Look For: The Barndominium Financing Checklist

Understanding what underwriters want makes the approval process much smoother. Here’s what matters most for barndominium financing in 2026:

✅ Permanent Foundation

Every major loan program requires this. A barndominium on piers, skids, or a non-permanent base will not qualify for conventional, FHA, VA, or USDA financing. You need a poured concrete foundation or equivalent — treated the same as any other residential mortgage property.

✅ Residential Classification

The property must be classified as residential, not agricultural or commercial. This often requires a zoning letter from your county. Work with your builder and county planning office early to confirm residential zoning.

✅ Licensed Contractor

Every government-backed loan program (FHA, VA, USDA) requires a licensed, insured general contractor. Owner-builder projects are generally limited to conventional loans or portfolio lenders.

✅ Detailed Construction Budget

Lenders need a complete, itemized construction budget — not a ballpark. Steel shell cost, insulation, electrical, plumbing, HVAC, interior finishing, site work, permits — all of it. Our barndominium cost guide breaks down every line item so you can build this document accurately.

✅ Comparable Sales (Comps)

The appraiser will try to find comparable barndominium sales in your area. This is easier in Texas, Oklahoma, and Tennessee than in, say, Connecticut. If comps are limited, a cost approach appraisal (what it would cost to rebuild the structure) may be used instead. Knowing this in advance helps set expectations.

✅ Credit Score and DTI

Most programs want a 640+ credit score; conventional lenders prefer 680–720+. Debt-to-income ratio (DTI) should generally be under 43% for government loans and under 45% for conventional. Our affordability calculator shows how your credit score affects your effective interest rate and maximum loan amount under real underwriting logic.

How Much Does Barndominium Financing Actually Cost?

Let’s run real numbers. Here’s a sample scenario for a 2,000 sq ft barndominium in Texas:

| Item | Amount |

|---|---|

| Land cost | $80,000 |

| Build cost (mid-range, $145/sqft) | $290,000 |

| Contingency (10%) | $29,000 |

| Closing costs (2.5%) | $9,750 |

| Total project cost | $408,750 |

At 20% down ($81,750), you’d be financing roughly $327,000. At a 7.25% permanent rate on a 30-year term, your principal and interest payment is approximately $2,232/month — before property taxes and insurance.

During construction (say, 9 months at 8.5% construction rate with an even draw schedule averaging 50% of the loan balance drawn), your interest-only payments would average approximately $1,156/month before the loan converts.

These numbers shift dramatically based on your state, credit score, draw schedule, and loan type. Texas barndominium costs per square foot, for example, differ from build costs in Tennessee or Minnesota — our Texas-specific cost breakdown goes deep on regional pricing.

For an instant estimate tailored to your specific inputs, the barndominium cost calculator handles all of this automatically.

Barndominium Financing vs. Traditional Home Loan: Key Differences

Many buyers come to barndominium financing expecting it to work like a standard home purchase mortgage. Here are the most important differences to understand upfront:

| Factor | Traditional Home Loan | Barndominium Construction Loan |

|---|---|---|

| Loan structure | Single disbursement at closing | Multiple draws during construction |

| Interest payments | Full P&I from day one | Interest-only on drawn amount during build |

| Appraisal basis | Comparable sales | Comparable sales or cost approach |

| Timeline | 30–60 days to close | 45–90 days to close, then 6–18 month build |

| Lender specialization needed | Low | High |

| Government-backed options | FHA, VA, USDA all widely available | Available but requires the right lender |

For a deeper dive into how barndominiums compare to traditional homes across cost, construction time, durability, and resale value, see our full barndominium vs. house comparison.

7 Mistakes That Kill Barndominium Financing Applications

Having worked through the mechanics, here are the most common reasons barndominium financing applications get denied or delayed — and how to avoid them.

1. Choosing the wrong lender first. Applying to a lender who has never done a barndominium loan wastes weeks and leaves a hard inquiry on your credit. Ask specifically: “Have you closed a barndominium construction loan in the last 12 months?” If the answer is no, move on.

2. Not confirming zoning early. Discovering that your land is agriculturally zoned after you’ve applied for residential financing is a common and painful surprise. Pull the zoning documentation before you engage any lender.

3. Owner-builder plans with government-backed loans. FHA, VA, and USDA all require a licensed contractor. If you plan to act as your own GC, you’re limited to conventional or portfolio lenders — and you need to know that from the start.

4. Underestimating the construction budget. Lenders look hard at construction budgets. If yours is unrealistically low, underwriters will flag it. Budget conservatively. Our barndominium cost guide shows real 2026 pricing so your numbers hold up to scrutiny.

5. Buying a kit before securing financing. Some buyers purchase a barndominium kit before their loan is approved. This can create complications — particularly with FHA and VA appraisals that need to evaluate the completed structure, not a stack of steel panels.

6. Ignoring insulation requirements. Certain loan programs — and virtually all building codes — have specific insulation requirements for residential properties. Spray foam insulation is increasingly the standard for barndominiums because it meets thermal and moisture requirements that lenders and inspectors expect. Our barndominium insulation guide explains what’s required and why.

7. Skipping the barndominium floor plan review. Lenders and appraisers evaluate your floor plans as part of underwriting. Poorly designed plans that don’t reflect residential use standards (no defined bedroom/bathroom layout, missing kitchen area) can raise red flags. See our floor plan design tips to make sure your plans hold up.

Barndominium Kits and Financing: What to Know

Pre-engineered barndominium kits are increasingly popular because they reduce construction time, simplify the building process, and often reduce material cost. But they create a specific financing question: can I finance a kit barndominium?

The short answer is yes — with the right approach. The key is that lenders aren’t financing the kit. They’re financing the completed residential structure. As long as:

- The kit is assembled by a licensed contractor

- The finished building meets residential code

- It sits on a permanent foundation

- It’s intended as your primary residence

…then standard barndominium financing options (C2P, FHA, VA, USDA) all remain available. The kit is simply one line item in your construction budget.

See our complete barndominium kits buying guide for a breakdown of top kit providers, costs, and what’s included — so you can incorporate accurate kit pricing into your construction loan application.

How to Choose the Right Barndominium Financing Option

Here’s a quick decision framework based on your situation:

You’re a veteran or active-duty military → Start with a VA construction loan. $0 down, no PMI, and the most favorable terms available. Find a lender experienced in VA barndominium loans specifically.

You’re building in a rural area and your income qualifies → USDA is your best bet for $0 down. Use the USDA eligibility map to confirm your property first.

Your credit score is below 680 → FHA construction loan. The 3.5% down requirement is manageable, and FHA’s credit flexibility is unmatched among government programs.

You have strong credit (700+) and 20% down → Conventional C2P loan or a local bank construction loan. You’ll get the best permanent rate and the fewest property restrictions.

You’re buying land and building simultaneously in a rural area → Farm Credit System lenders. They understand bundled land + construction financing better than anyone.

You’re not sure yet → Start with the barndominium cost calculator to nail down your total project cost. Then talk to at least three lenders — one local bank, one Farm Credit lender, and one specialist barndominium lender — before making a decision.

The Barndominium in 2026: Why Financing Is Getting Easier

There’s genuinely good news here. Barndominium financing in 2026 is meaningfully more accessible than it was even five years ago. Several factors are driving this:

More comparables exist. As more barndominiums get built and sold, appraisers have more data. Markets like Texas, Oklahoma, Tennessee, and the Carolinas now have enough barndominium sales history that appraisals are becoming more reliable.

Lender education has improved. Specialty lenders who understand post-frame and steel-frame construction have become more common. The Farm Credit System has expanded its residential barndominium programs. Some larger regional banks have developed dedicated barndominium loan products.

Building codes have caught up. Many counties that previously had no framework for residential post-frame construction have now adopted clear standards, making it easier to get permits and satisfy lender requirements.

Demand is sustained. With traditional home prices remaining elevated in most US markets, the cost advantage of barndominiums continues to attract buyers who would otherwise be priced out of rural homeownership. That sustained demand has pushed lenders to adapt.

For a complete picture of where barndominium design, cost, and construction stand in 2026, see our full barndominium guide for 2026.

Frequently Asked Questions: Barndominium Financing

Is it hard to get financing for a barndominium?

It’s not hard if you approach it correctly. The key is finding a lender with barndominium experience, ensuring your property is residentially classified, and using a licensed contractor. Applications fail most often due to the wrong lender choice, not the property itself.

What credit score do I need for barndominium financing?

USDA and FHA loans can go as low as 580–640. Conventional loans typically want 680+. VA loans are the most flexible, with no official minimum (though most lenders want 580–620+). Your credit score also affects your interest rate — see our affordability calculator for how this plays out in dollar terms.

Can I finance land and the barndominium together?

Yes, through a construction-to-permanent loan, Farm Credit lenders, or USDA/VA programs. The land value is typically included in the total loan amount, with your down payment calculated on the combined land + construction cost.

How long does barndominium construction financing take to close?

Expect 45–90 days from application to closing — longer than a standard home purchase due to the construction plan review, appraisal process, and draw schedule setup. Add 6–18 months for the build itself before the loan converts to a permanent mortgage.

Do I need mortgage insurance with a barndominium loan?

Conventional loans require PMI if your down payment is under 20%. FHA loans have mortgage insurance premiums (MIP) for the life of the loan (or 11 years if you put 10%+ down). VA loans have no PMI. USDA loans have an annual guarantee fee (0.35% of the loan balance) instead of traditional PMI.

Can I use a barndominium as a rental property or investment?

Most government-backed programs (FHA, VA, USDA) require the barndominium to be your primary residence. Conventional loans may allow investment use, but rates and requirements will be stricter. VA loans strictly require owner-occupancy.

Final Thoughts: Start With the Numbers

Barndominium financing doesn’t have to be complicated — it just has to be approached in the right order. Before you talk to a builder, before you pick a floor plan, and before you apply for any loan, run the numbers.

Know your total project cost. Know what your monthly payment will look like in both the construction phase and the permanent phase. Know how your credit score affects your rate. Know your debt-to-income ratio.

That clarity makes every conversation with a lender, builder, and real estate attorney more productive — and dramatically increases your chances of getting the right loan at the right rate for your barndominium.

The barndominium financing calculator at modernhouseplanideas.com handles all of this in one place: construction-phase interest by draw schedule, permanent mortgage payments, state-specific tax and insurance estimates, and credit score adjustments based on real underwriting logic. It’s free, it’s detailed, and it’s built specifically for barndominium projects.

Run your numbers, then go find your lender.

Published: May 2026 | modernhouseplanideas.com