Home Loan Calculator

Calculate your mortgage payment, check home affordability, compare FHA vs Conventional vs VA vs USDA loans, barndominium financing, and generate a full amortization schedule — all in one free tool.

Conventional

Best credit needed

FHA Loan

Low down, easy qualify

VA Loan

Veterans only, $0 down

USDA Loan

Rural, $0 down

Table of Contents

What Is a Home Loan Calculator and Why Do You Need One?

A home loan calculator is a free online tool that estimates your monthly mortgage payment based on your loan amount, interest rate, and loan term. But the best calculators like this one go far beyond a basic payment estimate.

This free mortgage calculator gives you five tools in a single page:

- True monthly cost — principal, interest, taxes, insurance, HOA, and PMI all included

- Affordability check — based on your income and debts, what’s the maximum home price you can comfortably buy?

- Loan type comparison — Conventional vs FHA vs VA vs USDA, side by side

- Barndominium financing — construction-stage cost breakdown for non-traditional builds

- Full amortization schedule — see every payment over the life of your loan, plus how extra payments slash interest

Whether you’re a first-time homebuyer just starting your search, or you’re deep in the mortgage process comparing offers from lenders, this calculator gives you the data you need to make a confident decision.

On a $350,000 home with a 7% interest rate, the difference between a 30-year and 15-year loan is over $160,000 in total interest. Use the calculator above to run your own numbers — the results might surprise you.

How to Use This Home Loan Calculator Step by Step

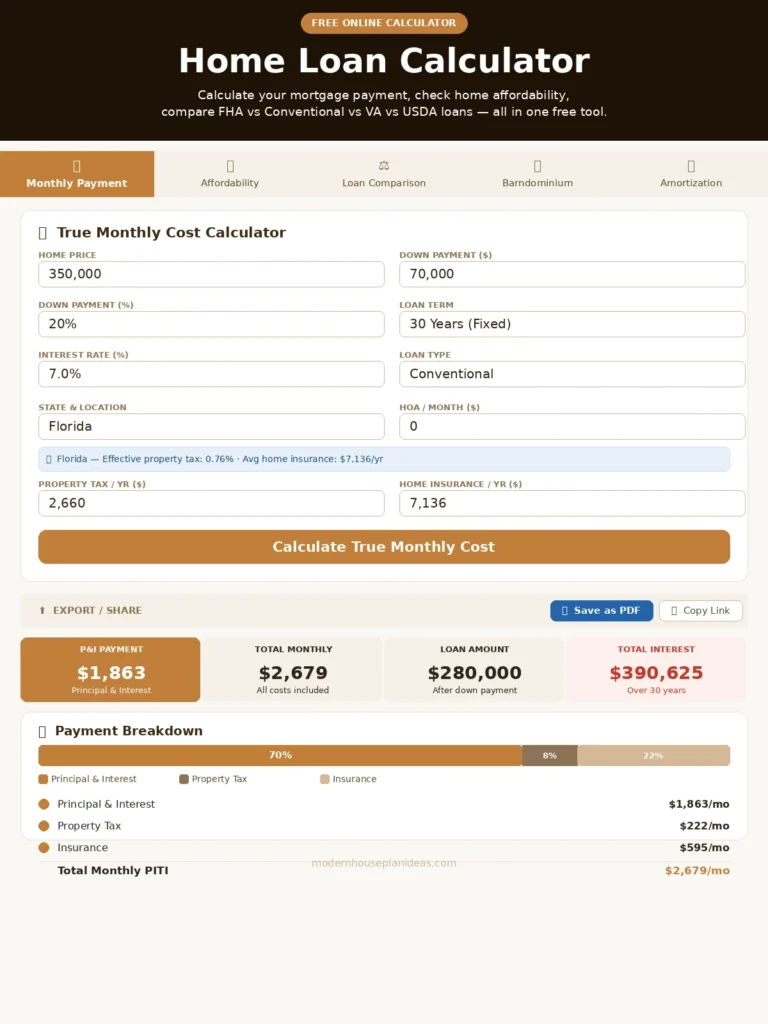

Step 1: Enter Your Home Price and Down Payment

Start with the home price you’re targeting and how much you plan to put down. The down payment calculator works both ways enter a dollar amount and the percentage auto-fills, or vice versa.

How much should you put down?

- 3% — Minimum for conventional loans (with PMI)

- 3.5% — Minimum for FHA loans

- 10% — Reduces PMI cost significantly

- 20% — Eliminates PMI entirely on conventional loans

- 0% — Available on VA and USDA loans for eligible buyers

Step 2: Choose Your Loan Term and Interest Rate

The calculator supports 10, 15, 20, and 30-year fixed terms. Your interest rate dramatically affects your monthly payment a 0.5% rate difference on a $300,000 loan equals roughly $90/month, or more than $32,000 over 30 years.

Step 3: Select Your State for Accurate Tax and Insurance Estimates

Property taxes vary enormously by state from under 0.3% in Hawaii to over 2.1% in New Jersey. Select your state and the calculator auto-fills realistic estimates. You can always override these with your actual figures.

Step 4: Add HOA Fees (If Applicable)

Homeowners Association fees are a real cost that many buyers forget to budget for. In planned communities and condos, HOA fees can range from $50 to $1,000+ per month. Enter your estimated HOA cost to get an accurate true monthly payment.

Step 5: Hit “Calculate” and Review Your Results

Your results show the complete payment breakdown with a visual chart. This home loan calculator displays your True Monthly Cost figure — not just the principal and interest lenders advertise. The True Monthly Cost figure is what you’ll actually budget for not just the principal and interest that lenders advertise.

FHA vs Conventional vs VA vs USDA: Which Home Loan Is Right for You?

One of the most valuable features of this home loan calculator is the ability to compare all four major loan types side by side. Here’s what you need to know before you run the numbers (source: HUD.gov):

| Loan Type | Min. Down | Min. Credit Score | Mortgage Insurance | Who Qualifies |

|---|---|---|---|---|

| Conventional | 3% | 620+ | PMI until 20% equity | Most buyers with good credit |

| FHA | 3.5% | 580+ (500 with 10% down) | MIP for life of loan (in most cases) | First-time buyers, lower credit scores |

| VA | 0% | No official minimum | No PMI (one-time funding fee) | Veterans, active military, surviving spouses |

| USDA | 0% | 640+ recommended | Small annual fee (lower than FHA) | Rural area buyers within income limits |

How Much House Can You Afford? Use the Affordability Calculator

The most common mistake first-time buyers make is working backward from a dream home price. Instead, start with the Affordability Calculator tab it tells you your actual budget based on your income and existing debts, using the same guidelines lenders use.

The 28/36 Rule Explained

Most mortgage lenders apply the 28/36 debt-to-income (DTI) rule. According to the Consumer Financial Protection Bureau (CFPB), DTI is one of the key metrics lenders use to determine how much you can borrow:

- Housing costs should not exceed 28% of your gross monthly income

- All monthly debts (housing + car loans + student loans + credit cards) should not exceed 36%

Example: If your household earns $90,000/year ($7,500/month), lenders typically want your total housing payment to stay under $2,100/month. With $400 in existing monthly debts, your max housing budget drops to around $2,300 based on the 36% total DTI limit.

Amortization Schedule — See Every Payment Over the Life of Your Loan

The Amortization Schedule tab in this home loan calculator shows you exactly how each monthly payment is split between principal and interest from your very first payment to your last.

Why the Amortization Schedule Matters

In the early years of a 30-year mortgage, the vast majority of your payment goes toward interest, not equity. On a $300,000 loan at 7%, your first payment of roughly $1,996 breaks down like this:

- Interest: ~$1,750

- Principal: ~$246

By year 15, that same payment is roughly split 50/50. By year 28, most of your payment is principal. The amortization table makes this visible so you can make smarter payoff decisions.

The Power of Extra Payments

The extra payment calculator inside the Amortization tab is one of its most powerful features. Here’s what a small extra monthly payment does on a $300,000 loan at 7%:

| Extra Monthly Payment | Interest Saved | Years Saved |

|---|---|---|

| $100/month | ~$28,000 | ~3.5 years |

| $200/month | ~$51,000 | ~6 years |

| $500/month | ~$100,000 | ~11 years |

Run your own numbers in the Amortization tab of this home loan calculator results update live based on your actual loan details.

Barndominium Loan Calculator — Financing a Non-Traditional Build

A barndominium is a metal building converted into or built as a residential home. They’ve exploded in popularity across rural America for their durability, lower cost-per-square-foot, and open floor plans. But financing one is more complex than a standard mortgage.

Before diving into financing, it helps to understand what you’re getting into cost-wise. Our detailed barndominium cost and design guide for 2026 walks through post-frame vs steel-frame builds, finishing stages, and realistic budget expectations from foundation to move-in.

How Much Does a Barndominium Cost?

Total build costs vary widely depending on size, location, and finish level. If you’re in Texas one of the most popular states for barndominium builds check our barndominium cost per square foot in Texas guide for current regional pricing. For a full state-by-state breakdown, our free barndominium cost calculator estimates your total build cost based on size, location, and finish options.

Not sure whether a barndominium is right for you vs a traditional stick-built home? Our barndominium vs house cost comparison breaks down real 2026 numbers on construction time, financing, durability, and resale value side by side.

Why Barndominium Financing Is Different

Most conventional lenders are reluctant to finance barndominiums because they’re harder to appraise there aren’t always comparable sales nearby. That means buyers often need to look at alternative financing paths:

- Construction-to-Permanent Loan — Covers the build phase, then converts to a permanent mortgage. Best for new builds.

- USDA Construction Loan — Available in eligible rural areas with no down payment required. Income limits apply. Check property eligibility at USDA’s eligibility map.

- Portfolio Loan — The lender keeps the loan in-house rather than selling it, giving them flexibility on non-standard properties.

- Conventional Loan — Possible if the barndominium meets standard appraisal criteria and has comparable sales nearby.

The Barndominium tab in this home loan calculator breaks down your estimated costs across all construction stages and compares monthly payments across each financing option.

Planning to Build? Additional Resources

Barndominium Planning Guides:

- How to plan a barndominium on a budget — Cost-saving strategies from shell to finish

- Best barndominium kits — buying guide and costs — Pre-engineered kit options vs custom builds

- Spray foam insulation for barndominiums — Why it’s the most critical finishing decision you’ll make

- How to design a barndominium floor plan — Layout tips for open-concept metal buildings

2026 Mortgage Rate Context

As of 2025, 30-year fixed mortgage rates have been in the 6.5%–7.5% range for most buyers, according to Freddie Mac’s Primary Mortgage Market Survey. The rate you get depends on your credit score, loan type, down payment, and lender. Here’s a general guide:

- Credit score 760+: Best available rates

- Credit score 720–759: ~0.25% higher than best

- Credit score 680–719: ~0.5%–0.75% higher

- Credit score 640–679: ~1%–1.5% higher

Always get quotes from at least 3 lenders. Even 0.25% lower rate saves $15,000+ on a $300k loan over 30 years.

7 Ways to Get a Lower Mortgage Rate

Once you’ve used this home loan calculator to see how rate changes affect your payment, here’s how to actually secure a better deal:

- Improve your credit score — Even 20–30 points can move you into a better rate tier. Pay down credit cards before applying.

- Increase your down payment — Lower loan-to-value ratio = lower risk for lenders = better rate offered.

- Shop at least 3 lenders — Rate variation between lenders on the same buyer can exceed 0.5%. Bankrate’s mortgage rate comparison tool is a free starting point before approaching lenders directly.

- Consider buying points — One discount point (1% of loan) typically lowers your rate by 0.25%. Worth it if you plan to stay 7+ years.

- Lock your rate quickly — Once you have an accepted offer, rates can move. A rate lock protects you for 30–60 days.

- Choose a 15-year term if you can afford it — 15-year rates are typically 0.5%–0.75% lower than 30-year rates.

- Use a local credit union — Credit unions often offer below-market rates on mortgages to their members.

Frequently Asked Questions

How do I calculate my monthly mortgage payment?

Enter your home price, down payment, loan term, and interest rate into the Monthly Payment tab above. The calculator instantly shows your principal and interest payment, then adds property taxes, homeowner’s insurance, HOA fees, and PMI for your complete true monthly cost.

What is the difference between FHA, VA, USDA, and Conventional loans?

Conventional loans require higher credit scores (620+) but have no mandatory mortgage insurance with 20% down. FHA loans allow lower down payments (3.5%) and are easier to qualify for but carry MIP for the life of the loan in most cases. VA loans are exclusively for eligible veterans and active military — no down payment, no PMI, and generally the lowest total cost. USDA loans offer zero-down financing for buyers in eligible rural areas with income limits. Use the Loan Comparison tab to see side-by-side monthly costs for your specific situation.

How much house can I afford on my salary?

A general rule: multiply your annual gross income by 2.5–3x for a rough maximum home price. For precision, use the Affordability Calculator tab. It applies the standard 28/36 debt-to-income rule lenders use — accounting for your income, existing monthly debts, down payment, and current interest rates.

What is PMI and when does it go away?

PMI (Private Mortgage Insurance) is required on conventional loans when your down payment is below 20%. It typically costs 0.5%–1.5% of the loan amount annually. Once you reach 20% equity through payments and/or home appreciation, you can request cancellation — lenders are required to remove it automatically when you reach 22% equity based on the original purchase price — this is mandated by the Homeowners Protection Act.

Is it better to get a 15-year or 30-year mortgage?

A 30-year mortgage has a lower monthly payment, giving you more cash flow flexibility. A 15-year mortgage has a higher monthly payment but a significantly lower interest rate and you pay roughly half the total interest over the life of the loan. The best choice depends on your income stability, other financial goals, and how long you plan to stay in the home. Use the Loan Term toggle in the Monthly Payment tab to compare both options instantly.

How do extra mortgage payments work?

Extra payments apply directly to your loan principal, reducing the balance faster and dramatically cutting total interest paid. Even $100/month extra on a typical mortgage saves tens of thousands in interest and cuts 3–4 years off a 30-year loan. Use the Amortization tab to calculate your exact savings based on any extra payment amount.

Can I finance a barndominium with a regular mortgage?

It depends on your location and the lender. In areas with comparable barndominium sales, a conventional appraisal may be possible. Otherwise, a construction-to-permanent loan, USDA loan (if in a rural area), or portfolio loan are the most common paths. The Barndominium Financing tab breaks down estimated costs and compares available loan types. For a full cost breakdown before you apply, use our barndominium cost calculator first.

Ready to Run Your Numbers?

Scroll back to the calculator above. It takes less than 60 seconds to get a complete picture of your mortgage costs — for free, with no email required.

Already used it? Share this page with a friend who’s thinking about buying a home. ↑